Are you looking for a way to get ahead of your credit card debt in 2025? Credit cards for balance transfers can be a smart solution. These cards allow you to move your existing credit card balance to a new card—usually with a low or 0% introductory interest rate. This can save you hundreds or even thousands of dollars in interest while giving you time to pay down your balance.

In this guide, we’ll break down the best credit cards for balance transfers in 2025. Whether you’re looking for no fees, long 0% APR offers, or perks like cashback or mobile app support, we’ve got you covered. Let’s jump in.

Contents

- 1 What Is a Balance Transfer Credit Card?

- 2 Benefits of Using Credit Cards for Balance Transfers

- 3 Key Factors to Consider

- 4 Best Credit Cards for Balance Transfers in 2025

- 5 How to Apply for a Balance Transfer Credit Card

- 6 Tips for Getting the Most from Balance Transfer Credit Cards

- 7 Common Questions About Balance Transfer Credit Cards

- 8 Final Thoughts

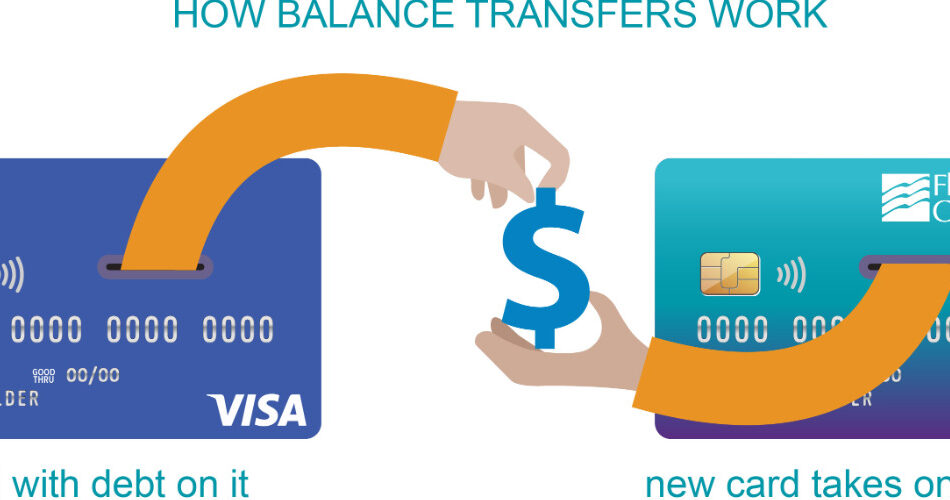

What Is a Balance Transfer Credit Card?

A balance transfer credit card is a type of credit card that lets you transfer existing debt from one or more credit cards to a new card—usually at a lower interest rate. Many of the best balance transfer cards offer 0% APR for an introductory period, often ranging from 12 to 21 months.

This gives you a window of time to pay off your balance without paying interest. Just be sure to watch for balance transfer fees, which are typically 3% to 5% of the amount transferred.

Benefits of Using Credit Cards for Balance Transfers

- Save on interest: With 0% APR offers, you can reduce or eliminate interest charges while paying down debt.

- Simplify payments: Consolidate multiple debts into one payment.

- Get out of debt faster: More of your payment goes toward the principal balance.

- Improve credit score: As you reduce debt and maintain on-time payments, your credit score may improve.

Key Factors to Consider

Before applying for a balance transfer credit card, consider these factors:

- Introductory APR period: Look for 0% APR offers that last 15+ months.

- Balance transfer fee: Some cards offer $0 transfer fees within the first 60 days.

- Ongoing APR: Know the rate that applies after the intro period ends.

- Credit requirements: Most top cards require good to excellent credit (670+).

- Perks and features: Some cards offer cash back, budgeting tools, or fraud protection.

Best Credit Cards for Balance Transfers in 2025

1. Chase Slate Edge™ Credit Card

Why it’s great: Long intro APR and no annual fee.

- Intro APR: 0% for 18 months on balance transfers

- Balance Transfer Fee: 3% (minimum $5)

- Ongoing APR: 19.24% – 27.99% variable

- Annual Fee: $0

Best for: People who want a long intro period without paying an annual fee.

2. Citi® Diamond Preferred® Card

Why it’s great: One of the longest 0% APR offers.

- Intro APR: 0% for 21 months on balance transfers

- Balance Transfer Fee: 5% (minimum $5)

- Ongoing APR: 18.24% – 28.99% variable

- Annual Fee: $0

Best for: Paying off larger balances over time.

3. Wells Fargo Reflect® Card

Why it’s great: Extended APR period and cell phone protection.

- Intro APR: 0% for up to 21 months (based on payments)

- Balance Transfer Fee: 3% for 120 days, then 5%

- Ongoing APR: 18.24% – 29.24% variable

- Annual Fee: $0

Best for: Those who need maximum time to pay down debt.

4. BankAmericard® Credit Card

Why it’s great: Simple card with no frills or distractions.

- Intro APR: 0% for 18 billing cycles on balance transfers

- Balance Transfer Fee: 3% (minimum $10)

- Ongoing APR: 16.24% – 26.24% variable

- Annual Fee: $0

Best for: Straightforward debt repayment with no extras.

5. Discover it® Balance Transfer

Why it’s great: Cashback + balance transfer.

- Intro APR: 0% for 18 months on balance transfers

- Balance Transfer Fee: 3% intro, then up to 5%

- Ongoing APR: 17.24% – 28.24% variable

- Annual Fee: $0

- Bonus: Cashback match in the first year

Best for: People who want to earn rewards while paying down debt.

How to Apply for a Balance Transfer Credit Card

- Check your credit score: Most cards require good credit.

- Compare offers: Look at APR, fees, and features.

- Apply online: Have your financial info ready.

- Transfer your balance: Do this soon after approval.

- Pay it off: Create a repayment plan before the intro period ends.

Tips for Getting the Most from Balance Transfer Credit Cards

- Transfer early: Most cards give you 60 days to complete a transfer.

- Avoid new purchases: They may not have the 0% APR.

- Don’t miss payments: You could lose the intro rate.

- Track your payoff goal: Aim to pay off the full balance before the intro APR expires.

- Use tools: Budgeting apps can help you stay on track.

Common Questions About Balance Transfer Credit Cards

Is there a limit to how much I can transfer?

Yes, it depends on your credit limit and the issuer’s policies.

Can I transfer a balance from the same bank?

Usually not. Most issuers won’t allow you to transfer balances between their own cards.

What happens after the 0% intro APR ends?

Your interest rate will jump to the regular APR. That’s why it’s important to pay off as much as possible during the intro period.

Will a balance transfer hurt my credit score?

It may cause a small dip due to the credit inquiry, but paying off debt can improve your score over time.

Final Thoughts

Using credit cards for balance transfers in 2025 is one of the smartest ways to reduce debt and save money on interest. The key is to pick the right card based on your financial needs—whether you want the longest intro APR, the lowest fees, or added perks.

Always read the fine print, make a solid repayment plan, and avoid adding new debt. With discipline and the right strategy, a balance transfer credit card can be your ticket to a debt-free future.

Ready to take control of your finances? Choose one of the best credit cards for balance transfers listed above and start saving today.