Debt can feel overwhelming, especially when you’re juggling multiple credit card payments, personal loans, or medical bills. If you’re looking for a simpler way to manage what you owe, debt consolidation may be the answer. But here’s the big question: how to consolidate debt without hurting your credit score?

It’s possible, and this guide will walk you through it—step by step. Whether you’re dealing with high-interest cards or personal loan debt, we’ll explain how to consolidate debt, manageable monthly payment while keeping your credit in good shape.

Contents

- 1 What Is Debt Consolidation?

- 2 Does Consolidating Debt Hurt Your Credit Score?

- 3 Step-by-Step: How to Consolidate Debt Without Hurting Your Credit

- 4 How to Maintain or Improve Your Credit During Consolidation

- 5 Debt Consolidation Mistakes to Avoid

- 6 Common Questions About Debt Consolidation

- 7 Tools and Resources to Help You Consolidate Debt

- 8 My Story: How I Consolidated Debt Without Damaging My Credit

- 9 Final Thoughts

- 10 Related Articles

What Is Debt Consolidation?

Debt consolidation means combining multiple debts into one new loan or credit account. The goal is to streamline payments, potentially reduce your interest rate, and pay off debt faster. There are several ways to consolidate debt:

- Personal loans

- Balance transfer credit cards

- Home equity loans or lines of credit (HELOCs)

- Debt management plans through nonprofit credit counselors

Each method has its pros and cons, and the best option for you depends on your financial situation and credit score.

Does Consolidating Debt Hurt Your Credit Score?

Consolidating debt can hurt your credit score temporarily, but it doesn’t have to if done correctly. Here’s how it might affect your score:

Potential Negative Impacts:

- Hard inquiries: When applying for a new loan or card, lenders do a hard credit pull.

- Average account age: Opening a new account lowers the average age of your credit history.

- New credit: Adding a new account increases your total number of open accounts.

Potential Positive Impacts:

- Lower credit utilization: Reducing high balances helps improve your credit score.

- Improved payment history: With one due date and less stress, you’re more likely to pay on time.

- Credit mix: Adding an installment loan (like a personal loan) can improve your credit mix.

Step-by-Step: How to Consolidate Debt Without Hurting Your Credit

Step 1: Check Your Credit Score

Start by checking your credit score with a free tool like Credit Karma, or directly through your credit card issuer. Your score will help determine which consolidation options are available to you.

- Good credit (670+): More likely to qualify for low-interest personal loans or 0% APR credit cards.

- Fair/poor credit (under 670): May need to consider a credit counseling program or secured loan.

Step 2: List All Your Debts

Create a list of your debts, including:

- Total amount owed

- Minimum monthly payment

- Interest rate

- Due date

This overview helps you understand what needs consolidating and allows you to compare it to consolidation options.

Step 3: Choose the Right Consolidation Method

Let’s break down the most popular ways to consolidate debt and how they affect your credit:

Option 1: Balance Transfer Credit Card

- Best for: High-interest credit card debt

- How it works: Transfer your balances to a card with 0% APR for 12-21 months

- Pros: Saves on interest, simplifies payments

- Cons: May charge a 3-5% transfer fee, requires good credit

- Impact on Credit: Minimal, if you don’t max out the new card and pay on time

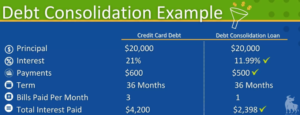

Option 2: Personal Loan

- Best for: Consolidating multiple types of debt

- How it works: Use the loan to pay off existing debts, then repay the loan monthly

- Pros: Fixed rate, fixed term, can improve credit mix

- Cons: Interest charges may apply, requires moderate-to-good credit

- Impact on Credit: Temporary drop from hard inquiry; improves over time with consistent payments

Option 3: Debt Management Plan (DMP)

- Best for: Those struggling to make minimum payments

- How it works: Work with a nonprofit counselor to negotiate lower interest and combine payments

- Pros: One monthly payment, reduced interest, support from counselor

- Cons: May close accounts, can take 3-5 years to complete

- Impact on Credit: Can hurt credit short-term, but helps long-term as debts are paid off

Option 4: Home Equity Loan or HELOC

- Best for: Homeowners with large amounts of debt

- How it works: Borrow against your home’s equity

- Pros: Lower rates than personal loans or credit cards

- Cons: Risk of losing your home if you can’t repay

- Impact on Credit: Similar to a personal loan; short-term dip, long-term gain

Step 4: Apply Carefully

Only apply for one consolidation method. Applying for multiple loans or cards within a short time can trigger several hard inquiries, which negatively affects your score.

- Compare offers on prequalification platforms

- Use soft-check tools when available

Step 5: Stick to a Repayment Plan

Once you’ve consolidated your debt, make it a top priority to stay on track. Set up automatic payments and budget around your monthly amount due.

- Avoid new credit card spending

- Build an emergency fund

- Track your progress using apps like Mint or YNAB

How to Maintain or Improve Your Credit During Consolidation

- Keep old accounts open: Don’t close old credit cards unless required

- Pay on time: Set up alerts or automatic payments to avoid late fees

- Don’t open new lines of credit unnecessarily

- Monitor your credit: Use free services to keep an eye on score changes and report errors

Debt Consolidation Mistakes to Avoid

- Applying for multiple loans at once

- Missing payments after consolidating

- Not checking fees and APR details

- Using new credit lines to rack up more debt

- Assuming consolidation is the same as debt elimination

Common Questions About Debt Consolidation

Is it better to consolidate debt or pay it off?

If you’re struggling to manage multiple payments or paying high interest, debt consolidation can help make payoff easier and faster.

Will my credit score go up if I consolidate my debt?

Yes—over time. If you reduce your credit utilization and maintain on-time payments, your score can increase.

How long does debt consolidation stay on your credit report?

The new loan or account will appear like any other and can stay for up to 10 years, depending on the account type.

Can I consolidate debt with a low credit score?

Yes, though your options may be limited. Consider credit union loans, secured loans, or a debt management plan.

Tools and Resources to Help You Consolidate Debt

- Credit score monitoring: Credit Karma,

- Loan comparison: LendingTree

- Budgeting tools: Mint, EveryDollar

- Credit counseling: NFCC.org (National Foundation for Credit Counseling)

My Story: How I Consolidated Debt Without Damaging My Credit

A couple of years ago, I found myself drowning in debt. I had maxed out three credit cards, taken out a personal loan to fix my car, and was struggling to make ends meet. My monthly payments were all over the place, and I could barely keep up.

I decided it was time to take control. After doing some research, I applied for a personal loan with a lower interest rate than my credit cards. I used it to pay off all my high-interest debts. At first, my credit score dipped slightly because of the hard inquiry and the new account, but I made sure to pay my new loan on time every month.

Within a year, my credit score improved significantly—from 660 to 725. I didn’t miss a single payment, and I avoided the temptation to use my newly freed-up credit cards. The experience taught me that consolidating debt can absolutely help if done with discipline and a plan.

Final Thoughts

If you’ve been wondering how to consolidate debt without hurting your credit score, now you know it’s all about choosing the right method and managing it wisely. From balance transfer credit cards to personal loans and counseling services, there are safe, effective ways to simplify your debt without damaging your financial future.

Be honest about your financial habits, explore the best ways on how to consolidate debt, read the fine print, and make consistent, on-time payments. With a smart strategy, you can use debt consolidation as a powerful tool to get out of debt—and even improve your credit score along the way.

Ready to take the first step? Start by checking your credit score and exploring how to consolidate debt.

Related Articles

- Best Credit Cards for Balance Transfers in 2025

- How to Choose the Best Online Accounting Degree

- 0 Interest Credit Cards vs Low APR Credit Cards: Which Is Better?

Stay informed and make smarter money moves—explore more guides and tips at Type For You.