If you’re considering taking out a loan, using a loan calculator can help you make smart, informed decisions. Whether you’re applying for a personal loan, car loan, student loan, or mortgage, understanding how much you’ll pay each month and how much the loan will cost you over time is essential.

We’ll explain how a loan calculator works, why it’s beneficial, and how to use it effectively before borrowing a single cent.

Contents

- 1 What Is a Loan Calculator?

- 2 Why You Should Use a Loan Calculator Before Borrowing

- 3 Step-by-Step: How to Use a Loan Calculator

- 4 Loan Calculator Tips & Tricks

- 5 Mistakes to Avoid When Using a Loan Calculator

- 6 Benefits of Using a Loan Calculator

- 7 Real-Life Examples: Using a Loan Calculator

- 8 FAQs About Loan Calculators

- 9 Final Thoughts: Why Every Borrower Needs a Loan Calculator

What Is a Loan Calculator?

A loan calculator is an online tool or app that helps you estimate the cost of a loan. It typically calculates monthly payments, total interest, and the overall amount you’ll pay back based on your loan details such as:

- Loan amount

- Interest rate

- Loan term (length of repayment)

- Down payment (if applicable)

These calculators are incredibly useful for comparing loan offers or understanding what you can afford.

Why You Should Use a Loan Calculator Before Borrowing

Here’s why using a loan calculator is a smart financial move:

- Clarity – Know exactly what your monthly payment will be.

- Comparison – Compare different loan options side-by-side.

- Budgeting – Ensure the monthly payments fit your financial plan.

- Interest Insight – Understand how much interest you’ll pay over time.

- Avoid Surprises – No more hidden costs or unclear terms.

When you take out a loan, it’s not just about how much you borrow – it’s about what it will cost you long-term. A loan calculator brings that information to light instantly.

Step-by-Step: How to Use a Loan Calculator

Let’s walk through exactly how to use a loan calculator to assess any loan scenario:

Step 1: Gather the Loan Details

Before you open the calculator, you’ll need the following details:

- Loan amount – The total amount you want to borrow.

- Interest rate – The annual interest rate (APR).

- Loan term – Number of months or years to pay off the loan.

- Down payment (if required) – Initial upfront payment.

- Fees – Any origination or processing fees.

These values are either provided by a lender or based on your research.

Step 2: Choose the Right Loan Calculator

Different types of loans require specific calculators. Here are the most common ones:

- Personal Loan Calculator

- Mortgage Loan Calculator

- Auto Loan Calculator

- Student Loan Calculator

Make sure you select a calculator designed for the loan type you’re considering.

Step 3: Enter Your Loan Amount

Input the total amount you plan to borrow. If you’re making a down payment, some calculators will ask for this separately.

Example: Loan amount = $20,000

Step 4: Input the Interest Rate

Enter the interest rate offered by your lender. This will be an annual percentage rate (APR).

Example: Interest rate = 6.5% APR

Step 5: Select Your Loan Term

Choose how long you want to repay the loan. This can range from 12 months to 30 years depending on the loan type.

Example: Loan term = 60 months (5 years)

Step 6: Review Monthly Payments

Once you hit calculate, the loan calculator will show you your estimated monthly payment. It will also often show you:

- Total interest paid

- Total amount paid back

Example Result:

- Monthly payment: $391.32

- Total interest: $3,479.20

- Total repayment: $23,479.20

Step 7: Adjust for Accuracy

Tweak the loan amount, term, or interest rate to see how it affects your monthly payments and total loan cost.

Want to pay less in interest? Try shortening the term. Want a lower monthly payment? Consider extending the loan duration (but you may pay more in interest overall).

Loan Calculator Tips & Tricks

Tip 1: Use Realistic Numbers

Always use the actual interest rate and fees provided by a lender, not a random estimate. This ensures your calculations reflect real-life scenarios.

Tip 2: Account for All Costs

Include taxes, insurance, and origination fees if applicable. Some calculators allow for extra fields.

Tip 3: Consider Prepayment Options

Some loan calculators let you add extra payments. See how prepaying can save you money over time.

Tip 4: Compare Multiple Scenarios

Use the calculator to compare various:

- Lenders

- Terms

- Loan amounts

- Interest rates

This helps you find the most cost-effective option.

Tip 5: Save or Print Results

If you’re planning to discuss loan options with a financial advisor or lender, bring your results to help guide the conversation.

Mistakes to Avoid When Using a Loan Calculator

Even the best tool is only as useful as the data you put into it. Here’s what not to do:

- Ignoring fees – Excluding loan origination or other fees skews your calculations.

- Using an incorrect interest rate – Always confirm the APR, not just the base rate.

- Not factoring insurance – Especially in mortgages or car loans, this adds cost.

- Focusing only on monthly payments – Consider total interest paid too.

- Failing to compare options – Never go with the first number you see.

Benefits of Using a Loan Calculator

Here’s a quick list of the biggest advantages:

- Increased transparency

- Better loan planning

- Fewer surprises down the road

- Time-saving comparisons

- Confidence when negotiating with lenders

Real-Life Examples: Using a Loan Calculator

Example 1: Auto Loan

- Loan Amount: $25,000

- Interest Rate: 4.5%

- Term: 5 years

Result:

- Monthly Payment: $466.08

- Total Interest: $2,964.80

- Total Cost: $27,964.80

Example 2: Personal Loan

- Loan Amount: $10,000

- Interest Rate: 9%

- Term: 3 years

Result:

- Monthly Payment: $318.08

- Total Interest: $1,451

- Total Cost: $11,451

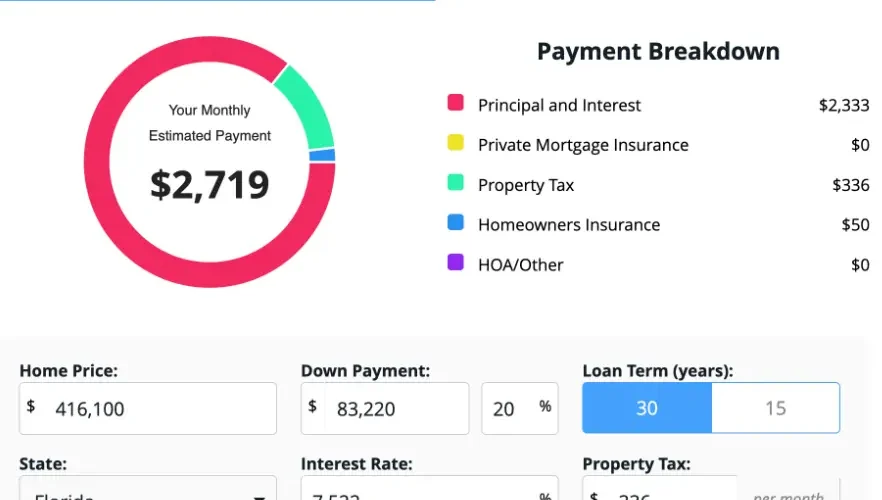

Example 3: Mortgage Loan

- Loan Amount: $250,000

- Interest Rate: 6%

- Term: 30 years

Result:

- Monthly Payment: $1,498.88 (excluding taxes & insurance)

- Total Interest: $289,596.80

- Total Cost: $539,596.80

These examples show how different loan amounts and terms impact your financial commitment.

FAQs About Loan Calculators

What types of loans can I calculate?

- Auto loans

- Personal loans

- Mortgages

- Student loans

- Business loans

Are loan calculator results accurate?

They’re estimates, but highly accurate when correct info is used. Always double-check with your lender.

Can I use a loan calculator for bad credit loans?

Yes! Just make sure to enter the correct higher interest rate typically associated with bad credit.

Are there mobile apps for loan calculators?

Yes, many financial institutions and budgeting apps offer mobile-friendly versions.

Final Thoughts: Why Every Borrower Needs a Loan Calculator

Using a calculator before borrowing is one of the smartest steps you can take to ensure you’re financially prepared. It helps you avoid overcommitting, understand your payments, and compare your options confidently.

Whether you’re financing a car, consolidating debt, or buying a home, this tool empowers you to borrow wisely. Never take a loan blindly let a loan calculator guide you toward smarter, more sustainable borrowing decisions.