In the world of finance, few indicators are as closely watched as the 10 treasury yield. It’s often used to gauge economic trends, investor sentiment, and even predict recessions. But what happens when the 10-year yield drops below the 2-year yield? This rare phenomenon is called a yield curve inversion, and it has investors, economists, and everyday savers paying close attention.

In this comprehensive guide, we’ll break down:

- What the 10 treasury yield is and how it works

- The difference between 10-year and 2-year treasury yields

- What a yield curve inversion means for the economy

- Why the inversion is seen as a recession signal

- How investors and consumers should react

Contents

- 1 What Is the 10 Treasury Yield?

- 2 What Is the 2-Year Treasury Yield?

- 3 Understanding the Yield Curve

- 4 10 Treasury Yield vs. 2-Year Yield: The Inversion Explained

- 5 What the Inversion Means for the Economy

- 6 Impact on Consumers

- 7 How Investors Should Respond

- 8 Inversion Isn’t a Crystal Ball

- 9 What Should You Do as a Consumer or Homeowner?

- 10 Frequently Asked Questions (FAQ)

- 11 Final Thoughts

What Is the 10 Treasury Yield?

The 10 treasury yield refers to the interest rate on the U.S. government’s 10-year bond. It’s considered a benchmark for long-term interest rates and is used as a key indicator in:

- Mortgage rates

- Auto loans

- Business investment decisions

- Stock market valuation

The yield is determined by demand: when more people buy 10-year bonds, prices go up and yields go down. When demand falls, yields rise.

Why the 10-Year Matters

The 10-year yield is widely followed because it reflects expectations for future economic growth and inflation. A high 10 treasury yield suggests optimism and potential inflation, while a low yield may indicate caution or economic slowdown.

What Is the 2-Year Treasury Yield?

The 2-year treasury yield is the interest rate on the U.S. government’s 2-year bond. It’s much more sensitive to short-term interest rate changes, especially those set by the Federal Reserve.

Why the 2-Year Matters

The 2-year yield is often viewed as a reflection of where the Fed might set interest rates in the near future. If inflation is rising, the Fed may increase interest rates, and the 2-year yield typically follows suit.

Understanding the Yield Curve

The yield curve is a graph that plots the yields of treasury securities ranging from short-term (like the 2-year) to long-term (like the 10-year). Normally, longer-term bonds have higher yields because investors expect a greater return for tying up their money longer.

Normal Yield Curve

- Short-term yields < Long-term yields

- Indicates economic expansion

Inverted Yield Curve

- Short-term yields > Long-term yields

- Often a sign of expected economic slowdown or recession

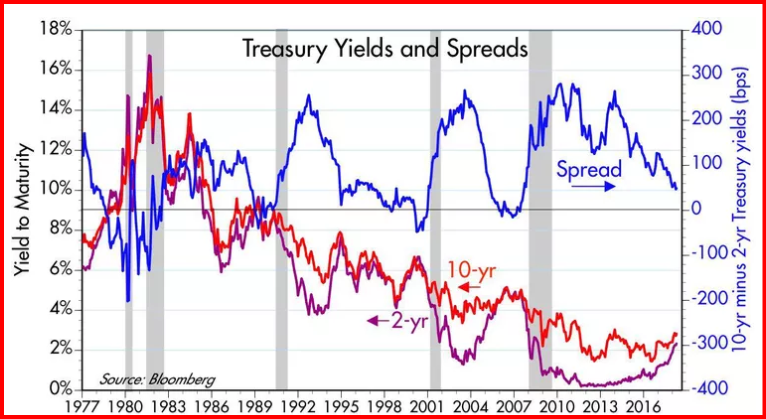

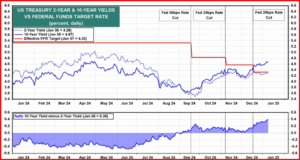

10 Treasury Yield vs. 2-Year Yield: The Inversion Explained

When the 10 treasury yield falls below the 2-year yield, it’s known as a yield curve inversion. This reversal of the norm is rare and is considered a potential red flag for the economy.

Why Does Inversion Happen?

There are several reasons:

- Investors expect a recession, so they flock to long-term bonds, increasing demand and lowering the 10-year yield

- The Fed raises short-term interest rates aggressively to combat inflation, pushing up the 2-year yield

- Market sentiment becomes risk-averse

Historical Context

Historically, an inversion of the 10-year and 2-year yields has preceded every U.S. recession over the last 50 years. While it doesn’t cause a recession, it has proven to be a reliable predictor.

What the Inversion Means for the Economy

1. Economic Slowdown Expected

An inverted curve signals that investors expect weaker economic growth and lower inflation in the future.

2. Recession Risk Rises

Many investors and analysts see the inversion as a warning that a recession could be on the horizon.

3. Business Investment May Slow

When long-term borrowing costs drop below short-term ones, it can hurt business planning and expansion.

Impact on Consumers

Mortgage Rates

Interestingly, while the Fed might raise short-term rates, mortgage rates can fall if the 10 treasury yield drops — making it cheaper to buy or refinance a home.

Credit Card and Loan Rates

These are often tied to short-term interest rates, which rise with the 2-year yield. That means consumers could face higher borrowing costs on credit cards, car loans, and personal loans.

How Investors Should Respond

1. Diversify Your Portfolio

In times of yield curve inversion, volatility increases. It’s smart to spread your investments across different asset classes (stocks, bonds, commodities, etc.).

2. Watch Defensive Stocks

Sectors like utilities, healthcare, and consumer staples often outperform during downturns.

3. Consider Bonds Wisely

Long-term bonds may look attractive, but understand the risk. Treasury Inflation-Protected Securities (TIPS) could offer some protection.

4. Monitor the Fed

Watch how the Federal Reserve reacts. Their monetary policy decisions will influence yields and the broader economy.

Inversion Isn’t a Crystal Ball

It’s important to note that not every inversion results in a recession — and the timing can vary. Sometimes a recession hits 12 to 24 months after the inversion. Other times, strong economic forces override the signal.

What Should You Do as a Consumer or Homeowner?

- Pay off high-interest debt while rates are still manageable.

- Lock in fixed mortgage rates if you’re planning to buy or refinance.

- Increase savings in high-yield savings accounts or CDs.

Frequently Asked Questions (FAQ)

What does it mean when the 10-year treasury yield is lower than the 2-year?

It means the yield curve has inverted, which signals that investors expect slower growth or a recession.

How often does a yield curve inversion happen?

It’s relatively rare and typically happens just before an economic downturn. It has occurred before every U.S. recession in the past 50 years.

Can you invest directly in the 10-year treasury bond?

Yes. You can buy U.S. Treasury bonds directly from TreasuryDirect.gov or through your brokerage.

Does the Fed control the 10-year yield?

Not directly. The Fed controls short-term interest rates, which influence the 2-year yield more. The 10 treasury yield is more influenced by market forces.

Final Thoughts

The 10 treasury yield is more than just a number — it’s a window into future economic expectations. When it dips below the 2-year yield, investors and economists take notice.

A yield curve inversion isn’t a guarantee of a recession, but it’s a strong warning sign. Whether you’re an investor, homeowner, or just trying to understand what’s going on with the economy, keeping an eye on the 10-year vs. 2-year yields can help you stay one step ahead.