The best business loans for small businesses include SBA loans, term loans, business lines of credit, and invoice financing. The right option depends on your needs SBA loans offer low rates, term loans provide large funding, lines of credit give flexibility, and invoice financing improves cash flow quickly.

Access to funding remains one of the biggest challenges for small businesses. Rising costs, tighter lending standards, and unpredictable markets mean that choosing the right business loan is more important than ever.

Whether you need capital to expand, manage cash flow, or invest in equipment, understanding your financing options can directly impact your success.

This guide breaks down the best business loans for small businesses, helping you compare options, understand requirements, and choose the right solution with confidence.

Contents

- 1 What Is a Business Loan?

- 2 Types of Business Loans for Small Businesses

- 2.1 1. SBA Loans (Best for Low Rates and Long-Term Financing)

- 2.2 Key Benefits:

- 2.3 Popular SBA Loan Options:

- 2.4 2. Term Loans (Best for Large One-Time Investments)

- 2.5 Key Benefits:

- 2.6 Typical Uses:

- 2.7 3. Business Line of Credit (Best for Flexibility)

- 2.8 Key Benefits:

- 2.9 4. Invoice Financing (Best for Cash Flow Issues)

- 2.10 Key Benefits:

- 3 How to Qualify for a Business Loan

- 4 How to Choose the Best Business Loan

- 5 Common Mistakes to Avoid

- 6 Final Thoughts

- 7 Bottom Line

What Is a Business Loan?

A business loan is a financing solution that allows companies to borrow money to support operations, growth, or investments.

Unlike personal loans, business loans are based on:

-

Business revenue

-

Creditworthiness

-

Financial performance

Small businesses use loans to:

-

Manage day-to-day cash flow

-

Purchase inventory or equipment

-

Expand operations

-

Cover unexpected expenses

With more lenders and digital platforms available in 2025, businesses now have more flexible and accessible funding options than ever before.

Types of Business Loans for Small Businesses

1. SBA Loans (Best for Low Rates and Long-Term Financing)

SBA loans are government-backed loans designed to support small businesses. Because they are partially guaranteed, lenders offer better terms and lower risk.

Key Benefits:

-

Lower interest rates

-

Longer repayment terms

-

Flexible use of funds

Popular SBA Loan Options:

-

SBA 7(a) Loans: Best for working capital, expansion, and refinancing

-

SBA 504 Loans: Ideal for real estate and large equipment

-

SBA Microloans: Up to $50,000 for startups and small businesses

👉 Best for: Businesses looking for affordable, long-term funding

2. Term Loans (Best for Large One-Time Investments)

Term loans provide a lump sum that is repaid over a fixed period with interest.

Key Benefits:

-

Predictable monthly payments

-

Higher loan amounts

-

Flexible usage

Typical Uses:

-

Expansion

-

Equipment purchases

-

Inventory investment

👉 Best for: Established businesses needing structured, long-term financing

3. Business Line of Credit (Best for Flexibility)

A business line of credit gives you access to funds up to a set limit. You can borrow, repay, and reuse funds as needed.

Key Benefits:

-

Borrow only what you need

-

Pay interest only on used funds

-

Reusable credit

👉 Best for: Managing cash flow and short-term expenses

4. Invoice Financing (Best for Cash Flow Issues)

Invoice financing allows you to borrow against unpaid invoices, giving you quick access to cash.

Key Benefits:

-

Fast funding (often within 24 hours)

-

No traditional collateral required

-

Improves cash flow instantly

👉 Best for: Businesses dealing with late-paying clients

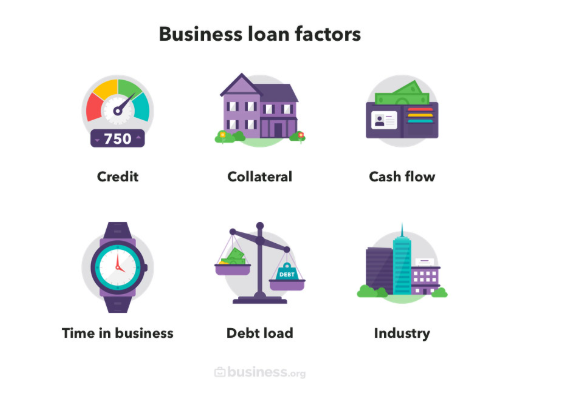

How to Qualify for a Business Loan

Lenders evaluate several key factors before approving a loan.

1. Credit Score

Your credit profile determines your approval chances and interest rates.

-

700+: Best rates and options

-

650–699: Good options available

-

Below 650: Limited options, higher rates

2. Business Revenue

Lenders want proof that your business can repay the loan.

-

Consistent income is critical

-

Minimum revenue requirements often apply

-

Profitability matters, not just sales

3. Time in Business

Most lenders prefer businesses with at least 1–2 years of history, although startups may qualify for specific loan types like microloans.

4. Collateral

Some loans require assets such as:

-

Equipment

-

Property

-

Inventory

Collateral reduces risk for lenders and can improve approval chances.

How to Choose the Best Business Loan

Selecting the right loan depends on your business goals and financial situation.

1. Define Your Needs

Ask yourself:

-

How much funding do I need?

-

What will the loan be used for?

Short-term needs = line of credit

Long-term investments = term loan or SBA loan

2. Compare Costs

Always review:

-

Interest rates

-

Fees

-

Total repayment cost

The cheapest loan is not always the best—but transparency matters.

3. Review Repayment Terms

Choose terms that align with your cash flow.

-

Fixed payments = stability

-

Flexible payments = adaptability

4. Check Lender Reputation

Work with lenders that offer:

-

Transparent terms

-

Positive reviews

-

Strong customer support

A reliable lender can make the entire process smoother.

Common Mistakes to Avoid

Many business owners make costly mistakes when choosing loans.

Avoid:

-

Taking more debt than needed

-

Ignoring hidden fees

-

Choosing the wrong loan type

-

Not comparing multiple lenders

Smart borrowing starts with informed decisions.

Final Thoughts

In 2025, small businesses have more financing options than ever—but not all loans are created equal.

The best business loans depend on your goals:

-

SBA loans for low-cost, long-term funding

-

Term loans for large investments

-

Lines of credit for flexibility

-

Invoice financing for cash flow

By understanding your options and preparing your financials, you can secure the right funding to grow your business with confidence.

Bottom Line

The right business loans can fuel growth, stabilize cash flow, and unlock new opportunities.

Choose wisely, plan strategically, and align your financing with your long-term vision and your business will be positioned to thrive in 2025 and beyond.

Categorized in: